Indeed, at some point in the years 2020 or 2021, China must formally declare that its economy is entering a cycle of successive contractions of its domestic product. This cycle can be brief and violent, like a shock, or it can be long and smooth; it all depends on the actions carried out by the Asian government authorities; and also, it will leave the Chinese economy in a period of stagnation that should last at least a decade. On the other hand, the rest of the economies of the planet will go into recession one after one after the collapse of the Asian giant and then, in the same way, culminate in a long period of stagnation. Finally, a small group of countries would not be entering the global contractive wave but would fall at once in the period of stagnation.

- determine if the company is able to withstand the consequences of the commercial war

- determine if the company has instruments to face the consequences of the commercial war.

These action plans should be based on absolutely objective arguments since the uncertainty situation favors confusion and misinformation. Indeed, it is expected that many media outlets dismiss the consequences of the commercial war, while the promoters of the US protectionist current are likely to sponsor the exacerbation of specific social movements, such as feminism, environmentalism or xenophobia; To distract public attention from the consequences of the commercial war, we can also anticipate that the government authorities of many nations will be very busy spreading calls for calm and proclaiming that they will protect their country's businesses from the effects of trade war when, in reality, this is impossible. If any company wishes to protect itself from the commercial war, it must base its actions based on objectivity and not on misinformation.

Go to: A Chinese recession is inevitable - don't think it won't affect you - Kenneth Rogoff - The Guardian

The instinctive reaction of the human being to a tragic situation is the denial of it. The negacionismo can take over a company, take it to the paralysis and demise. It is necessary that those who make the decisions in the company have all the information elements to conclude that the global recession is inevitable. Even in the case of a China-United States agreement there will be a global recession. The American protectionist discourse suggests that there is a commitment by the Trump Administration to reduce imports in a margin that would be between 30% and 50% at the end of the term.

- percentage of reduction in net sales for a given period of time

- number of time periods in which the reduction in net sales occurs.

We believe that this benchmark or starting point should be the "worst case scenario" of expected behavior of net sales. This scenario should be considered valid and applicable to all companies that could be affected by the commercial war. So, we think that the "worst possible scenario" for a company is the successive contraction of sales for five years in the following sequence: 10%, 10%, 10%, 5% and 5%. Then, from this starting point, each company will introduce the corresponding adjustments, dictated by common sense, until reaching the "specific scenario" that corresponds to the company. These adjustments will aim to reduce or maintain the number of periods of contraction of net sales and reduce the percentage values corresponding to each contract period.

So, it is the differentiation factors that allow the company to distance itself more and more from a planning scenario similar to the benchmark, that is, the "worst possible scenario." Some of these differentiation factors are:

- productive sector where the company is located: manufacturing, services, mining, etc.

- percentage of external sales with respect to total sales

- composition of the client portfolio

- composition of the group of suppliers, etc.

- the Chinese recession will be the trigger for the next global recession

- the Chinese recession is inevitable

- the Trump Administration has the inescapable commitment to the US protectionist current to reduce imports in a range that ranges from 30% to 50%

- the Chinese government will make all the efforts that are required so that the contractive rate never exceeds 5% per year

However, the entrepreneur, when carrying out his planning exercise, cannot consider that his sales will contract in a measure proportional to the contraction of the Chinese economy; nor can it be assumed that the company will go through the same amount of contraction periods as the Chinese economy should show. The entrepreneur must start his analysis from the "worst possible scenario", which should consider that the global economy now has abundant collateral factors that will increase the damage caused by the Chinese economic contraction to the global economy.

Obviously, the planning exercise carried out by the entrepreneur must quantify the sensitivity of his clients to the commercial war at the time of carrying out the projection of the magnitude of future sales, as well as measure the impact that the commercial war could cause on its suppliers in order to rule out possible threats to the supply chain that could jeopardize the company's operations.

|

| Global supply chain risk grows |

|

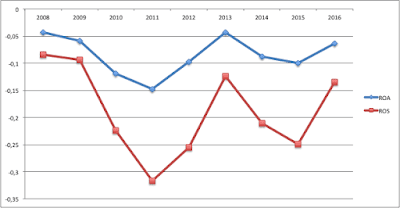

| Return on Asset and on Sales Volatility, that we measured with the standard deviation of the percentage change in operating income, after the peak reached in 2014, has settled on more moderate values in the last two years and close to those recorded in 2012 and 2013 |

Projected sales must include all discounts, price reductions, promotions and commercial strategy that the company deems to be carried out within the periods to be considered. On the other hand, the magnitude of the increase in average unit costs cannot be underestimated because it is an essential fact to reach the expected profit or loss. This information will be the fundamental input to design the corresponding plans and make the decisions that allow the company to survive the commercial war, hence the relevance in terms of data quality.

Indeed, the reduction in production will increase average unit costs by way of higher average unit fixed costs. Exporting companies usually have a considerable physical plant because export is a phenomenon that is more frequent in large companies; hence, we can determine that employers notice substantial increases in their average unit costs.

Non-North American exporting companies from all over the world will be affected, in one way or another, by the commercial war: reduction in profits or entry into the land of losses will be a constant within this group of companies. However, the corresponding government authorities of the countries where they come from should be implementing aid and incentives to them so that they do not close.